Demystifying Bonds And Bills: Uganda’s Opportunities Amid Regional Developments

Tuesday, February 17 2026 1:59 pm

By Julius Businge, Financial Journalist

Uganda’s government securities market is drawing growing attention from both domestic and foreign investors as treasury bills and bonds increasingly become central to the country’s financing strategy.

With yields on both short- and long-term government paper rising in recent months, the market is now at the center of conversations about inflation, debt sustainability, and the future of government borrowing.

The August 2025 auction, which included two, five, 15 and 25-year bonds, saw significantly higher pricing compared to earlier months. This reflects Uganda’s position as a higher-yield market within the region, attracting investors seeking better returns. However, these returns come with trade-offs. The higher yields signal tighter domestic financing conditions and reveal growing concerns over fiscal stability and the country’s mounting debt obligations.

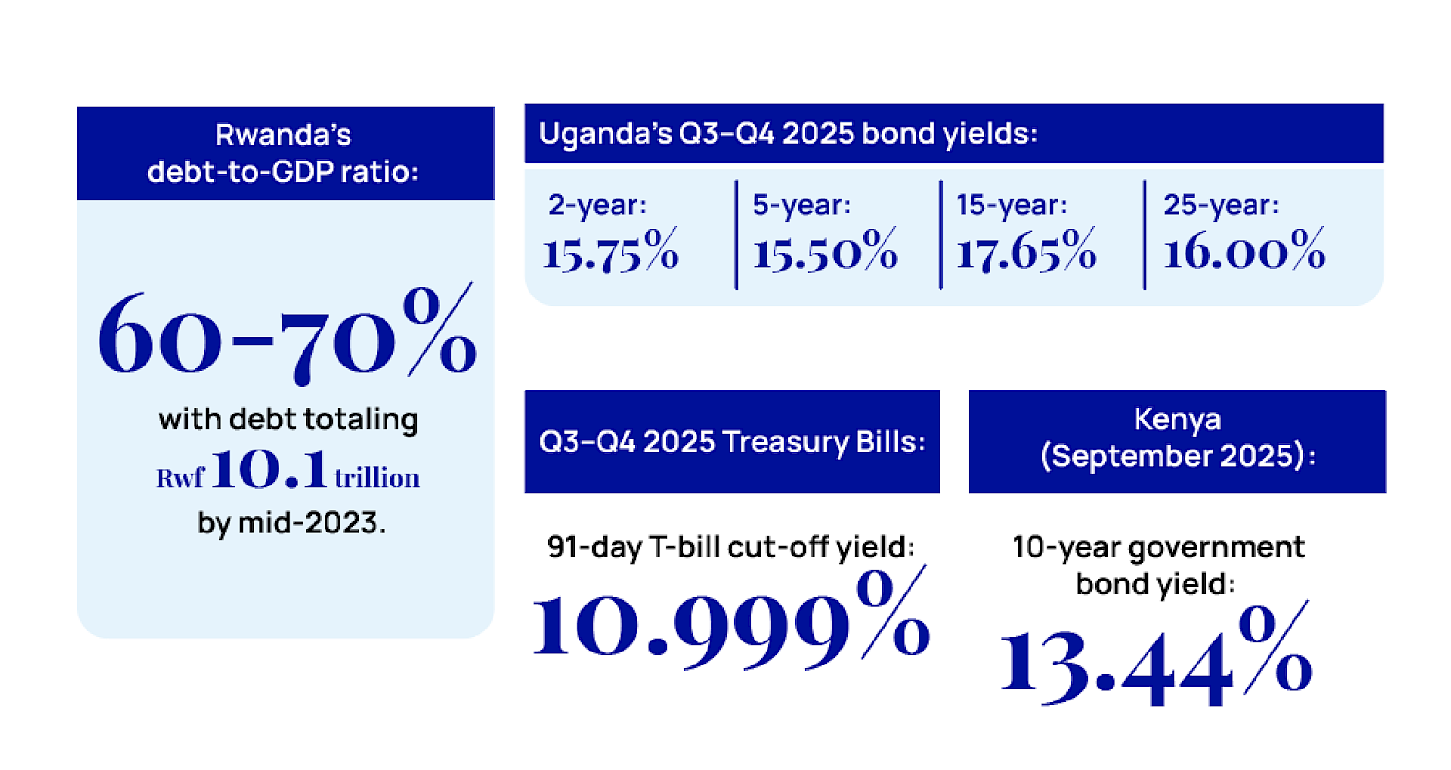

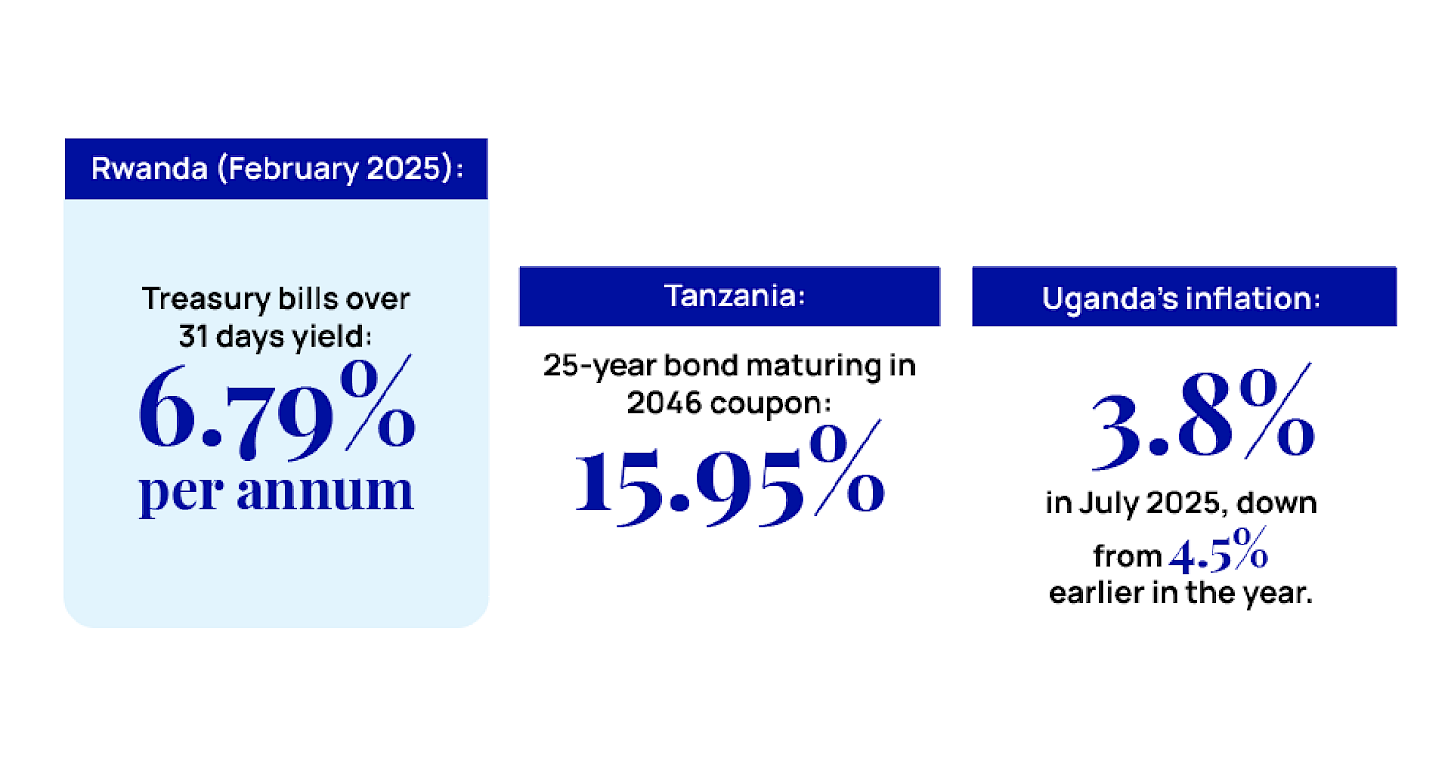

Comparatively, in August 2025, Uganda’s Treasury bond auction featured attractive coupon rates, with the 2-year bond at 14.125%, 10-year bond at 16.25%, 15-year bond at 15.8%, and 25-year bond at 16%. In Kenya, the latest 10-year government bond offers a 13.4% coupon, reflecting a more liquid but slightly lower-yielding market. Tanzania continues to offer high-carry opportunities, with one of its long-dated bonds, maturing in 2046, carrying a 15.95% coupon, according to Bank of Tanzania data. Rwanda’s smaller and niche government bond market offers coupon ranging between 8-9%, depending on maturity and demand.

Uganda’s rising debt

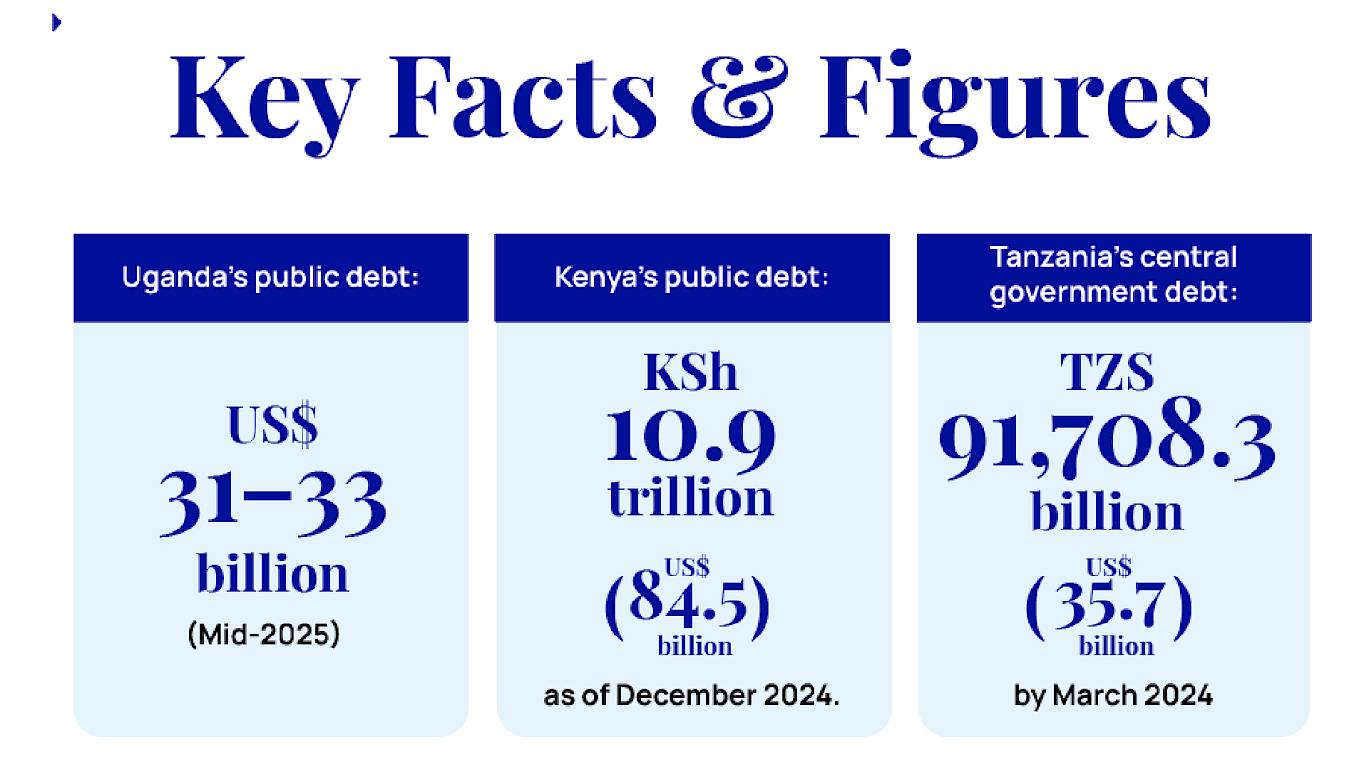

Uganda’s public and publicly guaranteed debt stood at US$31–33 billion by mid-2025, driven largely by rising domestic borrowing and longer-dated bond issuance. This represents a sharp rise compared to previous years, as the government has stepped up issuance to fund infrastructure projects and cover widening budget deficits.

In comparison, Uganda’s neighbors display different debt dynamics. Kenya, which operates the region’s most liquid securities market, had a debt stock of KSh 10.9 trillion (approximately US$84.5 billion) by December 2024. Tanzania reported central government debt of TZS 91,708.3 billion (US$35.7 billion) as of March 2024, while broader figures put its total debt slightly above US$40 billion, reflecting a growing domestic bond program supported by external concessional borrowing. Rwanda, meanwhile, has a smaller and shallower market, with its public debt rising to Rwf 10.1 trillion by mid-2023, representing a debt-to-GDP ratio of between 60 and 70 percent.

These numbers position Uganda between Kenya’s deep, highly liquid market and Tanzania’s higher-yielding, less liquid environment. Rwanda, on the other hand, represents a niche investment space, with fewer instruments but higher potential volatility.

“Many investors continue to view treasury bills as risk-free instruments, and Uganda must seize this opportunity to raise funds and finance its activities,” said John Walugembe, Head of the Federation of Small and Medium-Sized Enterprises, in an interview with this publication. He noted that Uganda’s relatively stable market could be a valuable tool for financing national development, provided policies encourage broader participation.

Politically driven borrowing

While Uganda’s bond market offers attractive yields, there are underlying structural concerns that cannot be ignored. Senior economist Fred Muhumuza warns that much of the country’s borrowing has been driven by political rather than economic considerations, especially as the country approaches another election cycle.

“The challenge is that public investment is being driven more by political expediency than economic necessity,” Muhumuza said in a televised show. “Many high-cost projects are being pushed through to win political favor rather than to meet urgent economic needs. This creates distortions in the bond and bill markets, as the government has to issue more paper to fund these expenditures.”

Muhumuza cautioned that Uganda is at risk of falling into a debt trap, where an increasing share of government revenue is spent on debt repayment rather than productive investments in health, education, or infrastructure. “In essence, Uganda is in a debt trap,” he said. “We are diverting resources away from essential sectors to pay for past borrowing. It’s unsustainable and puts upward pressure on yields, as investors demand higher returns to compensate for perceived fiscal risk.”

If government borrowing continues at the current pace, private-sector credit may become crowded out as commercial banks allocate more funds toward government securities. “We’ll see more of the government competing with the private sector for credit, which will drive up interest rates across the economy and undermine the very development objectives these borrowings are supposed to achieve,” he added.

Regional opportunities, risks

Across the East African region, each country’s bond market tells a different story. Kenya offers the deepest and most liquid market, allowing large institutional investors to move in and out with relative ease, though yields are lower. Tanzania provides attractive mid-teen coupon rates on its long-term bonds, which draw yield-seeking investors willing to accept less secondary market liquidity. Rwanda’s small market caters to specialized investors who adopt a buy-and-hold strategy, given its limited trading activity.

Dr. Enock Twinoburyo, a senior economist and advisor to regional governments, emphasized the importance of disciplined borrowing and strategic debt management. “Debt levels may be low in absolute terms, but the risks become insurmountable if borrowing is not disciplined and tied to productive investments,” he said. He noted that while Uganda’s high yields may attract investors, transparency and fiscal discipline will determine whether these opportunities are sustainable over the long term.

Twinoburyo explained that regional investors should consider East Africa not as a single uniform market but as a collection of distinct opportunities. Kenya’s strength lies in liquidity, Uganda’s in higher returns, Tanzania’s in long-term high coupons, and Rwanda’s in specialized, targeted investment potential. For investors with diversified strategies, combining exposure across these markets can balance yield, liquidity, and risk.

Growing domestic investor base

Walugembe believes that one of Uganda’s greatest opportunities lies in expanding domestic participation in the bond market. Currently, foreign investors dominate government securities, often repatriating profits abroad. Increasing local investment would keep more wealth circulating within the economy.

He pointed to Uganda’s low savings rate as a major obstacle but praised government backed initiatives such as SACCOs and Unit Trusts, which are designed to encourage broader participation in the financial system. However, he cautioned against policies that could discourage savers. “Introducing higher taxes on interest earned from these instruments could reverse progress by discouraging people from saving and investing,” he warned.

As Uganda’s ageing population steadily exits formal employment, treasury bills and bonds can provide a secure vehicle for individuals to grow their retirement savings.

The road ahead

The months ahead will be critical for Uganda’s bond market. The government’s ability to execute its FY2025/26 plan to reduce domestic borrowing will determine whether yields stabilize or continue rising. Across the region, other countries face their own pressures: Kenya is working to reduce its debt-to-GDP ratio, Tanzania is expanding its domestic bond program while managing external financing, and Rwanda is balancing ambitious infrastructure spending against debt sustainability concerns.

For investors, navigating these markets requires a careful blend of strategies. Those seeking liquidity may favor Kenya, while those looking for higher yields could focus on Uganda and Tanzania. Rwanda’s market remains suited for niche, patient investors.

East Africa’s bond and bill markets no longer present a uniform picture but rather a series of unique opportunities and challenges. If fiscal discipline and transparency are prioritized, these in struments could become engines of sustainable development rather than sources of economic instability.